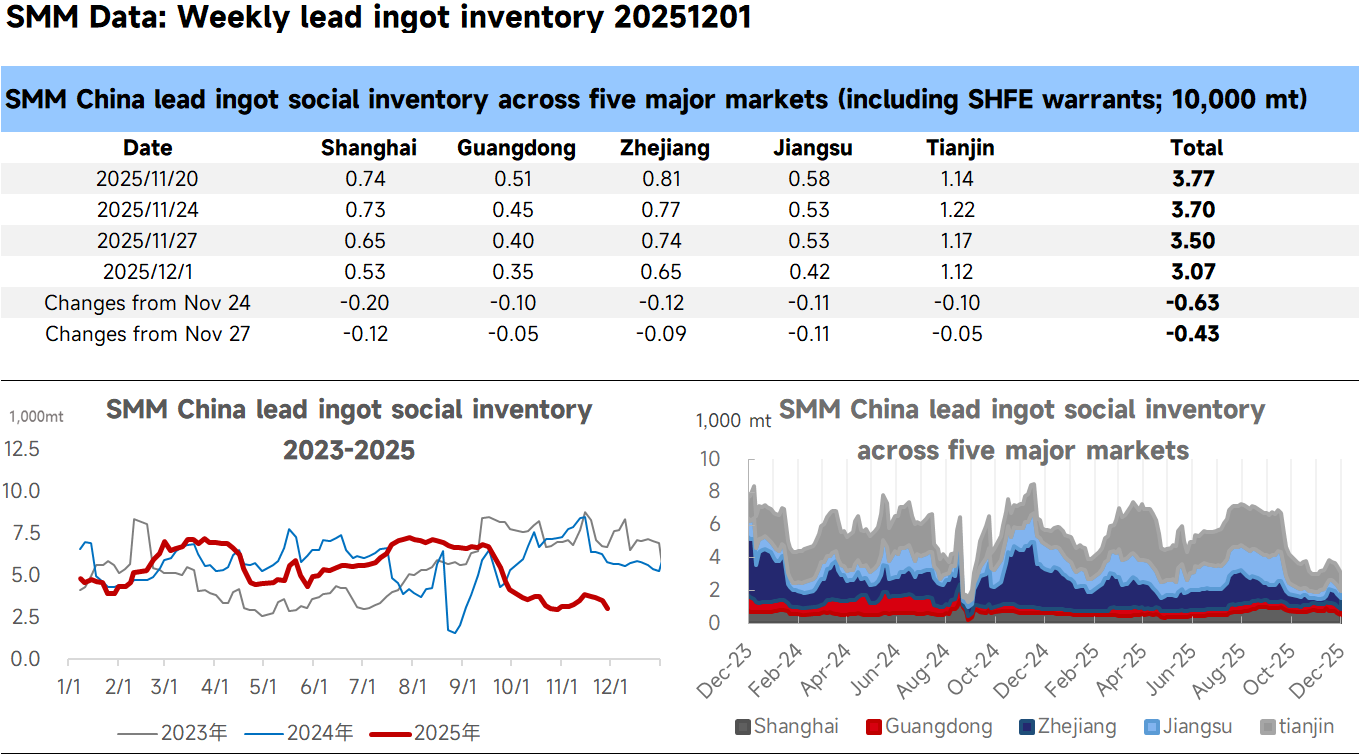

This week, primary lead smelters in regions such as Yunnan, Anhui, and Jiangxi were under maintenance, leading to tighter regional supply of lead ingots. Meanwhile, lead prices were in the doldrums, prompting smelters to hold back sales at lower prices. Quotations from major producing areas against the SMM #1 lead average price were at premiums of 0–100 yuan/mt ex-works. Secondary lead producers also held prices firm, with secondary refined lead quotations against the SMM #1 lead price at discounts of 50–0 yuan/mt ex-works, while more enterprises reported parity. Additionally, lead-acid battery production improved in December, with intentions to build inventory on price dips, leading to reductions in warehouse inventories around consumption areas and a further decline in social inventory of lead ingots. In December, maintenance and restarts coexisted among primary and secondary lead producers, but after offsetting production increases and decreases, a certain reduction in output is expected. With downstream enterprises purchasing as needed, short-term social inventory of lead ingots is expected to remain low.

Data Source Statement: Except for publicly available information, other data are processed by SMM based on public information, market communication, and SMM’s internal database model, for reference only and not as decision-making advice.